The current Stamp Duty holiday will remain in place until 30 June 2021 – an extension of three months, Chancellor Rishi Sunak has announced.

After this date, the nil rate band will be reduced to £250,000 until the end of September, and the usual level of £125,000 will return as of 1st October this year.

Mr Sunak said: “The cut in Stamp Duty I announced last summer has helped hundreds of thousands of people buy a home and supported the economy at a critical time.

“But due to the sheer volume of transactions we’re seeing, many new purchases won’t complete in time for the end of March.”

The move is also designed to help support jobs in the property sector. Mr Sunak said it’s estimated that 240,000 people are employed by house builders and their contractors, with a further 300,000 to 500,000 people in the supply chain.

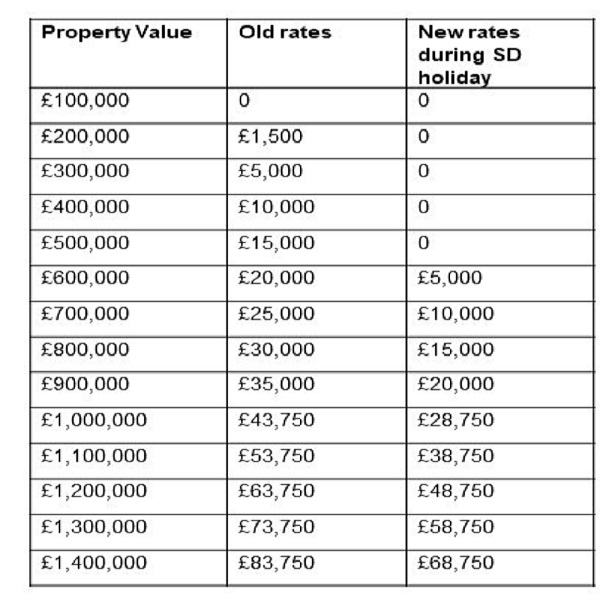

Stamp Duty explained

– Before the Stamp Duty holiday was announced last summer, only first-time buyers were exempt from paying the tax on properties costing up to £300,000. However, the introduction of the current scheme means that an exemption for all buyers applies to the first £500,000 of any residential property purchase. If a property is bought at under that amount no Stamp Duty is liable, and for purchases of over £500,000 there is a maximum saving available of £15,000 on any tax the buyer has to pay.

– On average, the scheme shaves around £2,000 from the cost of moving home for buyers in England and Northern Ireland on a property costing £249,633, the current UK average.

– However, from 1st July, the maximum saving available reduces from £15,000 to just £2,500 – a significant fall.

The Government’s annual take from stamp duty is usually around £12 billion, according to HM Revenue and Customs, which works out at around two per cent of all Treasury revenue.

Last summer, it was estimated the holiday would cost the Government an estimated £3.8 billion in lost tax revenue but that figure will now be higher given the extension to the end of June.

How much will I pay?

If the property purchased is your main home – and the sale is completed before 30 June – there won’t be any Stamp Duty payable at all if the property costs £500,000 or less.

The next portion of the property’s price (£500,001 to £925,000) will be taxed at 5%, and the £575,000 after that (£925,001 to £1.5m) at 10%.

The remaining amount (over £1.5m) will be taxed at 12%.

Landlords and second-home buyers are also eligible for the tax cut but will still have to pay the additional 3% of stamp duty they were charged under the previous rules.

Source: HM Revenue and Customs

Scotland and Wales

In Scotland, the normal rates on Land and Buildings Transaction Tax are:

2% on £145,001-£250,000

5% on £250,001-£325,000

10% on £325,001-£750,000

12% on any value above £750,000.

However, until the end of March, the threshold at which the tax starts to be paid was raised to £250,000, under measures brought in by the Scottish government. Landlords pay an extra 4% Land and Buildings Transaction Tax on top of standard rates.

In Wales, the normal rates on Land Transaction Tax are:

3.5% on £180,001-£250,000

5% on £250,001-£400,000

7.5% on £400,001-£750,000

10% on £750,001-£1.5m

12% on any value above £1.5m.

The Welsh government also introduced a temporary relief on the first tier, so until the end of March those buying their main home in Wales costing less than £250,000 do not pay any tax. Welsh landlords pay an extra 4% Land Transaction Tax on top of standard rates.

95% mortgages

The mortgage guarantee scheme was also announced in the Budget which will encourage lenders to offer 95% mortgages on the purchases of properties up to a value of £600,000, designed to make home ownership more accessible to those with a smaller deposit.

The pandemic has meant there were few low-deposit mortgages available, with just eight on the market in January 2021 compared to dozens the same time the previous year.

Mr Sunak said these mortgage products would be available from next month and won’t be restricted to first time buyers or new-build homes. High street lenders including Lloyds, NatWest, Santander, Barclays and HSBC will be launching them in early April, with other lenders such as Virgin Money following soon afterwards.

Other financial measures announced

– The furlough scheme is to be extended until the end of September, with higher employer contributions from July.

– Corporation Tax is to rise from 19 to 25 per cent in April 2023 for companies with profits of over £250,000. For businesses with profits of £50,000 or less, the current rate of 19% will remain, with a taper system in place for businesses with profits of between £50,000 and £250,000. This could impact landlords who hold their property portfolios in Special Purpose Vehicles (SPVs)

– Tax thresholds frozen until 2026, including Inheritance Tax

– £20 a week boost to Universal Credit will stay for another six months, alongside VAT and business rates for hospitality, leisure and tourism.