Floorplan

Floorplan Area stats

Area stats2 bedroom flat for sale

Key information

Features and description

- No chain

- 2 bedrooms

- Modern kitchen

- Modern bathroom with shower

- Lounge area with Juliette Balcony

- Double glazing

- Gas Central Heating

- 1st floor position

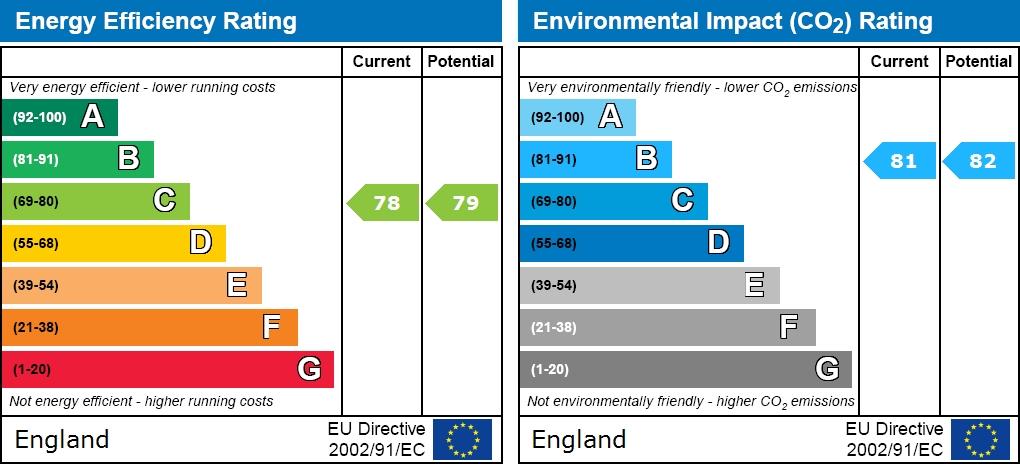

- EPC rating: C

- Property reference: 1000

Video tours

The property is offered with attractive window dressings, light fittings and solid oak flooring to the lounge and hallway areas.

Agents notes: The property is currently rented and being sold with no onward chain.

Tenure: Leasehold

Lease: 189 years from 2006 (approx 169 remaining).

Ground rent: £nil

Service charge: £2,200 most-recent demand.

Hours of business: We're open for business Monday - Friday 9.00am - 4.30pm.

Energy Performance Rating: 'C'.

Council Tax: Band 'B'. New Forest District Council (Totton & Eling Area) £1,744.21 for year 2024 / 2025.

Locality: Totton:

Some 3 miles West of Southampton, what used to be the largest village in England has grown to a population of nearly 30,000. However Totton and Eling is still considered a friendly place to live, with excellent shopping and leisure facilities, good schooling, from Infant to Secondary, and within a short drive of Lepe Country Park and a pebble beach at Calshot. Totton is served by the M27 (junctions 2 and 3) and a mainline Railway Station.

Directions: Starting from our offices at 1 Salisbury Road Arcade, Totton, Hampshire, SO40 3SG. Total : 0.1 miles (1mins)

1. Drive northwest. (0.08 miles)

2. Turn left onto Salisbury Road/A36. (0.02 miles)

3. You have arrived at your destination. (0.00 miles)

Hours of business: We're open for business Monday - Friday 9.00am - 4.30pm.

For further information or to view, please contact sole agents, Parkers Lettings Ltd on[use Contact Agent Button], quoting property reference 1000.

Understanding Stamp Duty: A Simple Explanation

Imagine you're buying a house it's a big purchase! Just like with some other things you buy, the government has a tax on buying property, and it's called Stamp Duty Land Tax (or just stamp duty for short). This tax applies if you're buying a home in England or Northern Ireland that costs more than £125,000. If you're buying in Wales or Scotland, they have their own similar taxes.

Think of the price of the house being divided into different chunks, or "bands." For each of these price chunks, there's a different percentage of tax you need to pay. It works a bit like this: you don't pay any tax on the very first bit of the price, but as the price goes higher, the percentage you pay on the extra bit also goes up.

How much is stamp duty?

Here's a breakdown of the different price bands and the tax rate for each, starting from April 1, 2025:

Price of the PropertyTax Rate

Up to £125,000:0%

£125,001 to £250,000: 2%

£250,001 to £925,000: 5%

£925,001 to £1.5 million: 10%

Let's look at an example:

Imagine you buy a house for £850,000 in April 2025. Here's how the stamp duty would be worked out:

On the first £125,000, you pay 0% tax = £0

On the next £125,000 (the part between £125,001 and £250,000), you pay 2% tax = £2,500

On the remaining £600,000 (the part between £250,001 and £850,000), you pay 5% tax = £30,000

So, the total stamp duty you'd owe is £0 + £2,500 + £30,000 = £32,500.

Who has to pay stamp duty?

Generally, if you're buying a residential (a place to live) property for more than £125,000, you'll need to pay stamp duty. There are different rules if you're buying a property that isn't just for living in, like a shop with a flat above it.

How do you pay stamp duty?

Usually, your solicitor (the legal person helping you with the house purchase) will handle all the paperwork and payment for you. You don't usually have to deal with it directly.

When do you pay stamp duty?

The stamp duty needs to be paid to the government within 14 days of when you officially become the owner of the property. Your solicitor should make sure this happens on time.

What about first-time buyers?

Yes, even if it's your first time buying a property, you still might have to pay stamp duty, but the rules are a bit different and can be more favorable for lower-priced homes. For example, if you buy a house for £500,000 as a first-time buyer in April 2025, you wouldn't pay any stamp duty on the first £300,000, and then you'd pay 5% on the remaining £200,000, which would be £10,000 in total. However, if the property costs more than £500,000, the regular stamp duty rules apply.

Are there any situations where you don't pay stamp duty?

There can be some situations where you might not have to pay stamp duty, or you might pay a different rate. For example, if you're buying a second home or a property to rent out (buy-to-let) from October 2024, you'll usually pay an extra 5% on top of the standard rates. Also, if you're not a UK resident, you might have to pay an extra 2% when buying a property in England or Northern Ireland.

Can you add stamp duty to your mortgage?

It might be possible to add the cost of stamp duty to your mortgage, but it depends on the mortgage lender. It's a good idea to speak to a mortgage advisor to see if this is an option for you.

Hopefully, this explanation makes stamp duty a bit clearer! Let us know if you have any other questions.

A bit about us: Here at Parkers, we know that you have many options to consider when it comes to choosing an agent, but we like to think that we offer you more than your standard agent. Were local specialists so when you want lettings, sales and property management services in Totton, Romsey and Southampton, we are second to none. We take immense pride in supporting the local community and playing our part in helping people take the next step in the market. Whether you need advice on where and when to buy-to-let, where to rent or you require assistance in reaching out to prospective buyers and tenants, we can help you. We place a strong emphasis on customer relationships, and we take the time to find out what you want to achieve.

If you're looking to sell your rented property, we're uniquely placed to help with our many hundreds of local landlords. By selling to another investor, it is often possible to keep your tenant in place, ensuring you receive rental income up to the very last day of your ownership, with the buyer receiving a return on their investment from the very next day. Our marketing comprises the best mix of technology, with video tours, floorplans and internet advertising, together with a nod to our heritage with good old fashioned estate agency practices.

Client Money Protection scheme membership : CMP003410 Property Redress Scheme membership : PRS002028

Rooms

Hallway 4.03m x 1.11m (13ft 2in x 3ft 7in)

Spacious and welcoming Hallway.

Living Room / Kitchen Area 3.14m x 5.64m (10ft 3in x 18ft 6in)

Living room

Solid oak flooring. Double-glazed French doors open on to Juliette Balcony. Open plan to:.

Kitchen area

A modern, re-fitted kitchen with integral oven, hob and extractor hood. Ample storage cupboards and work-surface space.

Bedroom 1 2.52m x 4.32m (8ft 3in x 14ft 2in)

Light and bright main bedroom, with built-in wardrobes.

Bedroom 2 2.03m x 4.91m (6ft 7in x 16ft 1in)

Good size second bedroom, again with built-in wardrobe.

Bathroom 2.39m x 1.69m (7ft 10in x 5ft 6in)

A modern, refitted white-coloured suite with shower over the bath wash-basin and WC.

External

Communal grounds to the front of the building. Bicycle store. On-road parking available nearby.